Selecionar segmento

Estude com questões de diferentes segmentos

Atenção: Isso limpará todos os campos já preenchidos no filtro!

Foram encontradas 3.725 questões

Resolva questões gratuitamente!

Junte-se a mais de 4 milhões de concurseiros!

Q1892826

Contabilidade Pública

De acordo com a NBC TSP 11 – Apresentação das Demonstrações

Contábeis, a entidade deve apresentar, na Demonstração do

Resultado ou nas Notas Explicativas, a análise das despesas

utilizando o detalhamento baseado na sua natureza ou na sua

função dentro da entidade, devendo selecionar o critério que

proporcione informação fidedigna e mais relevante.

São as seguintes as despesas classificadas de acordo com o método da função:

São as seguintes as despesas classificadas de acordo com o método da função:

Q1892825

Contabilidade Pública

De acordo com a NBC TSP Estrutura Conceitual – Estrutura

Conceitual para Elaboração e Divulgação de Informação Contábil

de Propósito Geral pelas Entidades do Setor Público, governos e

outras entidades do setor público devem prestar contas àqueles

que proveem os seus recursos.

De acordo com a norma, os doadores exigem informação principalmente para:

De acordo com a norma, os doadores exigem informação principalmente para:

Q1892824

Auditoria Governamental

A Instrução Normativa nº 84/2020 do Tribunal de Contas da

União (TCU) estabelece papéis e responsabilidades aos diversos

atores envolvidos no processo de tomada e prestação de contas

dos administradores e responsáveis da administração pública

federal, para fins de julgamento pelo TCU.

Esses papéis e responsabilidades estão corretamente descritos na seguinte opção:

Esses papéis e responsabilidades estão corretamente descritos na seguinte opção:

Q1892823

Auditoria

No desenvolvimento de um trabalho de asseguração sobre as

demonstrações contábeis de uma instituição pública, a equipe

realizou o processo de identificação e avaliação dos riscos de

distorção relevante do contexto auditado.

Em relação ao processo de avaliação e resposta aos riscos de distorção relevante, é correto afirmar que:

Em relação ao processo de avaliação e resposta aos riscos de distorção relevante, é correto afirmar que:

Q1892822

Auditoria

Uma equipe de auditoria foi estabelecida para realizar um

trabalho de asseguração sobre as demonstrações contábeis de

uma instituição pública referentes a 31/12/2021.

Em relação às características e aos procedimentos para a determinação da materialidade, é correto afirmar que:

Em relação às características e aos procedimentos para a determinação da materialidade, é correto afirmar que:

Q1892821

Auditoria Governamental

A materialidade está entre os princípios norteadores da

elaboração e divulgação da prestação de contas no âmbito da

Administração Pública Federal. Trata-se de um aspecto utilizado

para determinar a importância relativa de uma distorção ou

irregularidade, nível a partir do qual estas são consideradas

relevantes.

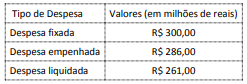

Nos termos da Instrução Normativa TCU nº 84/2020, para fins de autuação de processo de tomada de contas, é necessário avaliar o nível de materialidade.

Considere os dados do quadro a seguir relativos à execução orçamentária hipotética de uma autarquia federal no exercício financeiro de 2021.

O limite mínimo para que um conjunto de irregularidades detectadas na autarquia no referido exercício seja considerado materialmente relevante, para fins de autuação de processo de tomada de contas, é, em milhões de reais, de:

Nos termos da Instrução Normativa TCU nº 84/2020, para fins de autuação de processo de tomada de contas, é necessário avaliar o nível de materialidade.

Considere os dados do quadro a seguir relativos à execução orçamentária hipotética de uma autarquia federal no exercício financeiro de 2021.

O limite mínimo para que um conjunto de irregularidades detectadas na autarquia no referido exercício seja considerado materialmente relevante, para fins de autuação de processo de tomada de contas, é, em milhões de reais, de:

Q1892820

Auditoria Governamental

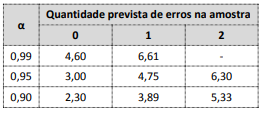

Durante um trabalho de auditoria, um dos procedimentos

previstos na matriz de planejamento era um teste de

conformidade (para controle de qualidade) em uma população

finita superior a 500 elementos. Para que a população testada

fosse aprovada, foi definido como critério que a proporção

máxima de erros admitidos seria de 3%. Foi considerado ainda

um nível de confiança de 95% e que a amostra conteria no

máximo um único erro.

Considere ainda a tabela a seguir, que contém índices calculados de confiabilidade para quantidades previstas de erros e níveis de confiança.

A partir dos dados apresentados e para cumprir os critérios previamente definidos, o tamanho da amostra para o teste na população indicada deve ser de:

Considere ainda a tabela a seguir, que contém índices calculados de confiabilidade para quantidades previstas de erros e níveis de confiança.

A partir dos dados apresentados e para cumprir os critérios previamente definidos, o tamanho da amostra para o teste na população indicada deve ser de:

Q1892819

Auditoria Governamental

O Tribunal de Contas da União adotou de forma adaptada

algumas ferramentas de auditoria utilizadas pelo U.S.

Government Accountability Office (U.S. GAO), a exemplo da

matriz de planejamento, que é uma ferramenta importante na

definição do escopo do trabalho de auditoria.

Na situação hipotética de um trabalho de auditoria que tem por objeto a concessão de auxílio financeiro emergencial a pessoas que perderam renda em decorrência de uma epidemia que atingiu o país e afetou a economia, a matriz de planejamento:

Na situação hipotética de um trabalho de auditoria que tem por objeto a concessão de auxílio financeiro emergencial a pessoas que perderam renda em decorrência de uma epidemia que atingiu o país e afetou a economia, a matriz de planejamento:

Q1892818

Auditoria Governamental

Nos trabalhos de auditoria, é necessária a definição de critérios,

que consistem em referências para avaliar o objeto auditado. Tais

referências são previamente determinadas pelo auditor.

No contexto das entidades públicas, conforme a ISSAI 100, a

definição desses critérios:

Q1892817

Engenharia de Software

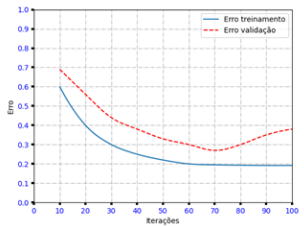

Durante o treinamento de uma rede neural artificial para

classificação de imagens, foi observado o comportamento

descrito pelo gráfico abaixo, que mostra a evolução do erro

conforme o número de iterações.

O classificador em questão foi treinado em um conjunto de dados particionado (holdout) em 60%/30%/10% (treinamento/validação/ teste). Entretanto, os especialistas envolvidos consideraram o modelo obtido insatisfatório após analisarem o gráfico.

Considerando essas informações, duas técnicas que poderiam ser utilizadas para contornar o problema encontrado são:

O classificador em questão foi treinado em um conjunto de dados particionado (holdout) em 60%/30%/10% (treinamento/validação/ teste). Entretanto, os especialistas envolvidos consideraram o modelo obtido insatisfatório após analisarem o gráfico.

Considerando essas informações, duas técnicas que poderiam ser utilizadas para contornar o problema encontrado são:

Q1892816

Engenharia de Software

Uma organização está implementando um sistema de busca de

informações interno, e a equipe de desenvolvimento resolveu

avaliar diferentes modelos de linguagem vetoriais que ajudariam

a conectar melhor documentos e consultas em departamentos

que usam terminologias distintas em áreas de negócio que se

sobrepõem. Um dos analistas ressaltou que seria interessante

guardar os vetores de todo o vocabulário do modelo em um

cache, de forma a aumentar a eficiência de acesso e reduzir

certos custos de implantação.

Das alternativas abaixo, aquela que lista apenas os modelos compatíveis com essa estratégia de caching é:

Das alternativas abaixo, aquela que lista apenas os modelos compatíveis com essa estratégia de caching é:

Q1892815

Direito Digital

Conjuntos de dados identificados de pessoas são úteis em

pesquisas, ao mesmo tempo que são motivo de preocupação em

relação à privacidade das pessoas naturais envolvidas. A

classificação de atributos identificadores ajuda a priorizar

atividades de desidentificação para alavancar a pesquisa sob a

observância da LGPD.

São exemplos: a) de identificadores explícitos, b) de identificadores sensíveis e c) de quasi identificadores:

São exemplos: a) de identificadores explícitos, b) de identificadores sensíveis e c) de quasi identificadores:

Q1892814

Governança de TI

A universidade YEDU implantou um sistema ERP (Enterprise

Resource Planning) no final da década de 1990. Ao longo dos

anos, foram feitas diversas customizações para atender novas

demandas de negócio. Após um tempo, tornou-se evidente uma

disparidade de dados na YEDU. Um mesmo aluno era visto em

até seis sistemas. Para agravar ainda mais essa disparidade, os

nomes e os atributos dos alunos foram preenchidos com diversos

erros de digitação em cada sistema. Os sistemas de BI não

possuíam recursos para mostrar uma visão única de cada aluno.

A alta administração da YEDU decidiu então implementar um programa de Gestão e Governança de Dados. Para resolver o problema de repetições de dados de alunos na YEDU, o CDO (Chief Data Officer) definiu corretamente a seguinte abordagem:

A alta administração da YEDU decidiu então implementar um programa de Gestão e Governança de Dados. Para resolver o problema de repetições de dados de alunos na YEDU, o CDO (Chief Data Officer) definiu corretamente a seguinte abordagem:

Q1892813

Algoritmos e Estrutura de Dados

Considere os documentos A e B a seguir.

A = “Há pessoas que choram por saber que as rosas têm espinho” B = “Há outras que sorriem por saber que os espinhos têm rosas”

A submatriz da matriz de TF-IDF desses dois documentos correspondente aos termos “Rosas”, “Choram” e “Sorriem”, nessa ordem, é:

A = “Há pessoas que choram por saber que as rosas têm espinho” B = “Há outras que sorriem por saber que os espinhos têm rosas”

A submatriz da matriz de TF-IDF desses dois documentos correspondente aos termos “Rosas”, “Choram” e “Sorriem”, nessa ordem, é:

Q1892812

Programação

A tabela presente no código em R abaixo apresenta a quantidade

de processos analisados por três analistas (denotados por A1, A2

e A3) em diferentes anos.

dados = tibble::tibble(Analista=c(“A1”, “A1”, “A1”, “A2”, “A2”, “A3”, “A3”, “A3”),

Ano=c(2018,2019,2020,2019,2020,2018,2019,2020), Processos=c(10,15,20,25,20,8,7,12))

Um programador roda o código abaixo em R.

tidyr::pivot_wider(data=dados, names_from=”Analista”, values_from=”Processos”)

Os valores esperados na primeira linha do objeto resultante do comando acima são:

dados = tibble::tibble(Analista=c(“A1”, “A1”, “A1”, “A2”, “A2”, “A3”, “A3”, “A3”),

Ano=c(2018,2019,2020,2019,2020,2018,2019,2020), Processos=c(10,15,20,25,20,8,7,12))

Um programador roda o código abaixo em R.

tidyr::pivot_wider(data=dados, names_from=”Analista”, values_from=”Processos”)

Os valores esperados na primeira linha do objeto resultante do comando acima são:

Q1892811

Banco de Dados

Um analista do TCU gostaria de aplicar um modelo de Latent

Dirichlet Allocation (LDA) em um conjunto de textos. A alternativa que melhor descreve o resultado do modelo é:

Q1892810

Banco de Dados

Um analista de dados deseja criar um modelo para classificação

de documentos em duas categorias: sigilosos e públicos. À sua

disposição, existe um conjunto de dados com N documentos, dos

quais uma fração α deles é sigilosa. O analista quer escolher uma

fração β dos N documentos para pertencer ao conjunto de teste.

O objetivo é garantir que cada uma das classes (documentos

sigilosos e públicos) seja responsável, em média, por ao menos

10% do total de documentos. Essa restrição precisa ser válida

tanto no conjunto de treino quanto no conjunto de teste.

Um par (α,β) que satisfaz as restrições do analista é:

Q1892809

Engenharia de Software

Seja uma rede neural com camada de entrada com dimensão dois

que recebe dados (x1

, x2

). Essa rede aplica pesos w1 em x1

, w2 em

x2 e adiciona um viés w0

. A função de ativação é dada pela função

sinal s(z) = +1, se z ≥ 0, e s(z) = -1, se z < 0. Essa rede não tem

nenhuma camada oculta e será utilizada para classificar

observações em y=+1 ou y=-1.

Para pesos w1 = 2, w2 = 3 e viés w0 = 1, a região de classificação é uma reta que passa nos pontos:

Para pesos w1 = 2, w2 = 3 e viés w0 = 1, a região de classificação é uma reta que passa nos pontos:

Q1892808

Banco de Dados

Em um problema de classificação é entregue ao cientista de

dados um par de covariáveis, (x1

, x2

), para cada uma das quatro

observações a seguir: (6,4), (2,8), (10,6) e (5,2). A variável

resposta observada nessa amostra foi “Sim”, “Não”, “Sim”,

“Não”, respectivamente.

A partição que apresenta o menor erro de classificação quando feita na raiz (primeiro nível) de uma árvore de decisão é:

A partição que apresenta o menor erro de classificação quando feita na raiz (primeiro nível) de uma árvore de decisão é:

Q1892807

Banco de Dados

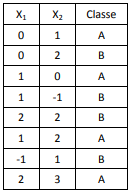

Um analista do TCU recebe o conjunto de dados com

covariáveis e a classe a que cada amostra pertence na tabela a

seguir.

Esse analista gostaria de prever a classe dos pontos (1,1), (0,0) e (-1,2) usando o algoritmo de k-vizinhos mais próximos com k=3 e usando a distância euclidiana usual.

Suas classes previstas são, respectivamente:

Esse analista gostaria de prever a classe dos pontos (1,1), (0,0) e (-1,2) usando o algoritmo de k-vizinhos mais próximos com k=3 e usando a distância euclidiana usual.

Suas classes previstas são, respectivamente: