Questões de Concurso

Para fiscal

Foram encontradas 9.996 questões

Resolva questões gratuitamente!

Junte-se a mais de 4 milhões de concurseiros!

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956767

Banco de Dados

Uma Secretaria da Fazenda Estadual está reestruturando seu modelo de governança de dados fiscais. Atualmente, três áreas

distintas gerenciam dados tributários: a Coordenadoria de Fiscalização, a Subsecretaria de Arrecadação e a Diretoria de

Tecnologia da Informação. Cada área mantém seus próprios padrões de qualidade, políticas de acesso e definições de

metadados, gerando inconsistências nas análises. Para resolver o problema, a alta administração decidiu criar uma estrutura de

governança onde representantes das três áreas se reúnem periodicamente para deliberar sobre políticas, padrões e prioridades

relacionadas aos dados tributários. As decisões sobre frameworks de qualidade, taxonomias de metadados e diretrizes de

acesso são tomadas através de votação pelos membros, com cada área tendo poder de voto proporcional ao volume de dados

sob sua responsabilidade. Adicionalmente, foram estabelecidos padrões corporativos mínimos obrigatórios, enquanto cada área

mantém autonomia para decisões operacionais específicas de seus processos internos, desde que em conformidade com os

padrões aprovados pelo grupo deliberativo.

Nesse caso, a governança de dados implementada foi

Nesse caso, a governança de dados implementada foi

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956766

Estatística

Uma Secretaria da Fazenda Estadual precisa analisar 500 mil declarações fiscais para identificar contribuintes com comportamento tributário similar, sem ter exemplos prévios de classificação. A equipe técnica deve agrupar as empresas considerando

apenas as características declaradas (receita, despesas, setor, localização) e descobrir padrões naturais nos dados.

A técnica mais adequada para essa tarefa é:

A técnica mais adequada para essa tarefa é:

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956765

Governança de TI

Determinada Secretaria da Fazenda implementou um sistema de IA para classificar automaticamente declarações fiscais quanto

ao risco de irregularidade. Após seis meses de operação, auditores identificaram que o modelo estava atribuindo pontuações de

risco sistematicamente mais altas para empresas de setores específicos, mesmo quando os indicadores financeiros eram

similares aos de outros setores com pontuações menores. A análise técnica revelou que a base de dados histórica utilizada no

treinamento continha proporcionalmente mais autuações em determinados setores devido a fiscalizações direcionadas

realizadas no passado, e não necessariamente por maior incidência real de irregularidades. O modelo aprendeu e perpetuou

esse padrão desproporcional. O problema de governança e ética em IA que está caracterizado nessa situação é:

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956764

Banco de Dados

A Secretaria da Fazenda de determinado Estado implementou uma solução corporativa para centralizar dados fiscais provenientes

de múltiplas fontes heterogêneas: declarações de contribuintes, notas fiscais eletrônicas, dados cadastrais e informações de fiscalizações. A equipe técnica precisava garantir escalabilidade, processamento de grandes volumes e capacidade analítica para identificar irregularidades tributárias. Após análise, optou-se por uma arquitetura que permite armazenar dados brutos em formato nativo, aplicar transformações sob demanda mediante ferramentas de processamento distribuído e disponibilizar estruturas otimizadas

para consultas analíticas pelos auditores fiscais, mantendo a governança através de controles transacionais sobre os metadados.

A arquitetura implementada

A arquitetura implementada

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956763

Banco de Dados

Uma Secretaria da Fazenda Estadual recebeu uma base de dados contendo 2,3 milhões de registros de declarações fiscais para

análise de conformidade tributária. Durante a fase de exploração inicial, a equipe técnica identificou diversos problemas: campos de

CNPJ com formatações inconsistentes (alguns com pontuação, outros sem), valores monetários registrados com separadores

decimais divergentes (vírgula e ponto), datas em formatos distintos (DD/MM/AÄAA, AAAA-MM-DD), campos obrigatórios vazios em

aproximadamente 12% dos registros, e a presença de valores extremos de receita bruta (outliers) que distorciam as análises

estatísticas. Além disso, a variável "regime tributário" apresentava categorias redundantes devidoa erros de digitação (ex:

"Simples Nacional", "SIMPLES NACIONAL", "Simples nacional"). Para viabilizar a análise de risco fiscal e a construção de modelos

preditivos, tornou-se necessário aplicar técnicas sistemáticas de preparação dos dados antes do processamento analítico.

Considerando as melhores práticas de pré-processamento de dados, o tratamento correto e adequado para essa situação é

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956762

Banco de Dados

Um sistema estadual de arrecadação consolida diariamente indicadores tributários provenientes de múltiplas fontes e, para acelerar

leituras repetitivas desses indicadores já consolidados, a equipe de Dados está avaliando armazená-los em um banco NoSQL do

tipo chave-valor. Considerando as características desse modelo de dados, a justificativa que melhor fundamenta essa escolha é:

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956761

Banco de Dados

No desenvolvimento de um modelo de detecção de contribuintes com alto risco de simulação de operações, após definir claramente com a área de fiscalização quais tipos de fraude serão priorizados, quais indicadores de negócio serão acompanhados

(como aumento de autos de infração qualificados e redução de fiscalizações improdutivas) e quais restrições legais e

operacionais existem para uso do modelo, a equipe de uma Secretaria da Fazenda registra esses critérios e alinha expectativas

com a alta gestão. Com base na metodologia CRISP-DM, essa descrição se encaixa principalmente na fase de

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956760

Segurança da Informação

Uma Secretaria da Fazenda verificou que os acessos às declarações de contribuintes são registrados na mesma tabela de

negócio, podem ser alterados por DBAs e que registros antigos são apagados para liberar espaço. A fiscalização pediu um

redesenho que aumente a integridade e a rastreabilidade dos acessos às declarações, sem prejudicar a disponibilidade do

sistema. Nesse cenário, o redesign que atente à exigência de integridade e rastreabilidade forte é

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956759

Direito Digital

Um órgão fazendário estadual fiscaliza o transporte de cargas e mantém bases de NF-e e declarações tributárias com dados

pessoais e sensíveis. A legislação tributária fixa prazos mínimos de guarda, enquanto a LGPD permite retenção apenas pelo

tempo necessário e sob certas condições para fins estatísticos. Encerrados os prazos legais, o órgão quer seguir fazendo

análises estatísticas de longo prazo. Nesse cenário, a política de retenção e descarte que atende a esses requisitos é:

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956758

Banco de Dados

Uma equipe de fiscalização deseja gerar um relatório priorizando contribuintes cujo volume de NF-e emitidas seja atípico. A

tabela nfe contém, entre outras, as colunas contribuinte id e qtd_emitidas. Deseja-se listar os contribuintes cuja

quantidade emitida no mês seja maior que 5000 ou menor que 10, ordenando a saída do maior para o menor valor de

qtd_emitidas. O comando SQL que atende ao requisito é:

SELECT contribuinte_id,

SELECT contribuinte_id,

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956757

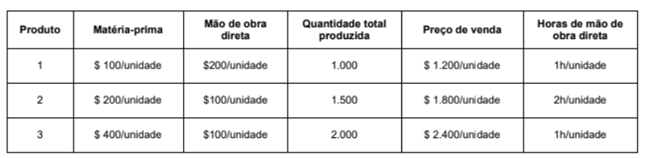

Contabilidade de Custos

A empresa Emagreça & Beleza produz 3 medicamentos utilizando um único departamento. Ao analisar o processo produtivo no

mês de janeiro de 2025, a empresa obteve as seguintes informações:

A empresa utiliza o método de custeio por absorção e aloca os custos indiretos aos produtos em função da quantidade de horas de mão de obra direta utilizada. Sabendo que os custos indiretos totais incorridos, no mês de janeiro de 2025, totalizaram R$ 1.800.000 e que não havia estoques iniciais e finais de produtos em processo, os custos unitários de produção, no mês de janeiro de 2025, para os produtos 1, 2 e 3 foram, respectivamente, em reais,

A empresa utiliza o método de custeio por absorção e aloca os custos indiretos aos produtos em função da quantidade de horas de mão de obra direta utilizada. Sabendo que os custos indiretos totais incorridos, no mês de janeiro de 2025, totalizaram R$ 1.800.000 e que não havia estoques iniciais e finais de produtos em processo, os custos unitários de produção, no mês de janeiro de 2025, para os produtos 1, 2 e 3 foram, respectivamente, em reais,

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956756

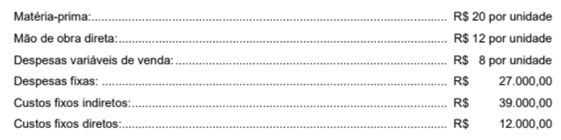

Contabilidade de Custos

No mês de dezembro de 2025, uma empresa produziu 3.000 unidades do seu único produto e, para a produção dessas unidades, incorreu nos seguintes gastos:

Sabendo que a empresa adota o método de custeio por absorção, que o preço unitário de venda praticado pela empresa é R$ 600, que os impostos sobre a venda correspondem a 10% do preço de venda, que a empresa paga comissões de venda de 5% do preço de venda por unidade vendida, que não havia estoque inicial e que foram vendidas 1.200 unidades, o

Sabendo que a empresa adota o método de custeio por absorção, que o preço unitário de venda praticado pela empresa é R$ 600, que os impostos sobre a venda correspondem a 10% do preço de venda, que a empresa paga comissões de venda de 5% do preço de venda por unidade vendida, que não havia estoque inicial e que foram vendidas 1.200 unidades, o

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956755

Contabilidade de Custos

Texto associado

Atenção: Utilize os dados a seguir para responder à questão.

A empresa industrial Canecas S.A. produz um único produto e, para produzir integralmente 5.000 unidades desse produto,

incorreu nos seguintes gastos durante o mês de janeiro de 2026:

• Custos fixos: R$ 30.000

• Custos variáveis:

• Matéria-prima: R$ 8/unidade

• Mão de obra direta: R$ 6/unidade

• Despesas fixas: R$ 15.000

• Despesas variáveis: R$ 4/unidade

• Comissões de venda: 10% do preço de venda

Informações adicionais:

• Preço de venda: R$ 60/unidade

• Impostos sobre a Venda: 10% da receita de vendas

• Quantidade vendida: 2.000 unidades

O ponto de equilíbrio da empresa industrial Canecas S.A., em unidades vendidas, é:

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956754

Contabilidade de Custos

Texto associado

Atenção: Utilize os dados a seguir para responder à questão.

A empresa industrial Canecas S.A. produz um único produto e, para produzir integralmente 5.000 unidades desse produto,

incorreu nos seguintes gastos durante o mês de janeiro de 2026:

• Custos fixos: R$ 30.000

• Custos variáveis:

• Matéria-prima: R$ 8/unidade

• Mão de obra direta: R$ 6/unidade

• Despesas fixas: R$ 15.000

• Despesas variáveis: R$ 4/unidade

• Comissões de venda: 10% do preço de venda

Informações adicionais:

• Preço de venda: R$ 60/unidade

• Impostos sobre a Venda: 10% da receita de vendas

• Quantidade vendida: 2.000 unidades

Sabendo que a empresa industrial Canecas S.A. utiliza o Método de Custeio por Absorção, o custo unitário da produção do

período foi, em reais,

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956753

Contabilidade Geral

Em 01/12/2025, a empresa Sonhos & Cia. obteve um empréstimo no valor de R$ 10.000.000 com as seguintes características:

• Prazo total: 8 anos.

• Taxa de juros compostos: 11% ao ano.

• Pagamentos: parcelas iguais e anuais de R$ 1.943.210,54, com vencimento em 01 de dezembro.

Para a obtenção do empréstimo, a empresa incorreu em custos de transação no valor total de R$ 571.927,00, pagos no ato da assinatura. Sabendo que a taxa de custo efetivo da emissão foi de 1% ao mês (equivalente a 12,68% ao ano), a empresa Sonhos & Cia

• Prazo total: 8 anos.

• Taxa de juros compostos: 11% ao ano.

• Pagamentos: parcelas iguais e anuais de R$ 1.943.210,54, com vencimento em 01 de dezembro.

Para a obtenção do empréstimo, a empresa incorreu em custos de transação no valor total de R$ 571.927,00, pagos no ato da assinatura. Sabendo que a taxa de custo efetivo da emissão foi de 1% ao mês (equivalente a 12,68% ao ano), a empresa Sonhos & Cia

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956752

Contabilidade de Custos

Para produzir seu único produto, a empresa Só Indústria S.A. incorreu nos seguintes gastos durante o mês de dezembro de 2025:

• Compra de matéria-prima: R$ 50.000 (líquido dos tributos recuperáveis)

• Fretes e seguros para transporte das matérias-primas até a fábrica: R$ 2.500 (não inclusos no valor da matéria-prima acima).

• Mão de obra direta: R$ 12.000

• Remuneração da supervisão da fábrica: R$ 15.000

• Aluguel do galpão industrial: R$ 21.000

• Remuneração da administração geral da empresa: R$ 26.000

• Depreciação dos ativos utilizados na produção: R$ 9.000

• Comissão dos vendedores: R$ 5.000

• Outros custos indiretos de produção: R$ 7.000

• Materiais consumidos na administração geral da empresa: R$ 2.500

• Encargos financeiros de empréstimos obtidos: R$ 3.000

O estoque inicial de matéria-prima era R$ 6.000, o estoque final R$ 4.500 e não havia estoque de produtos em elaboração no início e no fim de dezembro de 2025. Sabendo que os gastos da administração geral da empresa não são rateados para o setor de produção, o custo da produção acabada no período utilizando o custeio por absorção foi, em reais,

• Compra de matéria-prima: R$ 50.000 (líquido dos tributos recuperáveis)

• Fretes e seguros para transporte das matérias-primas até a fábrica: R$ 2.500 (não inclusos no valor da matéria-prima acima).

• Mão de obra direta: R$ 12.000

• Remuneração da supervisão da fábrica: R$ 15.000

• Aluguel do galpão industrial: R$ 21.000

• Remuneração da administração geral da empresa: R$ 26.000

• Depreciação dos ativos utilizados na produção: R$ 9.000

• Comissão dos vendedores: R$ 5.000

• Outros custos indiretos de produção: R$ 7.000

• Materiais consumidos na administração geral da empresa: R$ 2.500

• Encargos financeiros de empréstimos obtidos: R$ 3.000

O estoque inicial de matéria-prima era R$ 6.000, o estoque final R$ 4.500 e não havia estoque de produtos em elaboração no início e no fim de dezembro de 2025. Sabendo que os gastos da administração geral da empresa não são rateados para o setor de produção, o custo da produção acabada no período utilizando o custeio por absorção foi, em reais,

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956751

Contabilidade Geral

Considere:

I. O uso de estimativas razoáveis é parte essencial da elaboração de demonstrações contábeis e não reduz sua confiabilidade.

II. São exemplos de estimativas contábeis: ajuste para perdas esperadas de crédito, valor líquido realizável de um item de estoque e despesa de depreciação para um item do ativo imobilizado.

III. Os efeitos de mudanças nas estimativas contábeis são reconhecidos nas demonstrações contábeis de forma prospectiva, a partir da data dessa mudança.

IV. A entidade deve corrigir os erros materiais de períodos anteriores de forma retrospectiva, a partir da data em que tal erro foi identificado, salvo quando for impraticável determinar os efeitos específicos do período ou o efeito cumulativo do erro.

Está correto o que se afirma em

I. O uso de estimativas razoáveis é parte essencial da elaboração de demonstrações contábeis e não reduz sua confiabilidade.

II. São exemplos de estimativas contábeis: ajuste para perdas esperadas de crédito, valor líquido realizável de um item de estoque e despesa de depreciação para um item do ativo imobilizado.

III. Os efeitos de mudanças nas estimativas contábeis são reconhecidos nas demonstrações contábeis de forma prospectiva, a partir da data dessa mudança.

IV. A entidade deve corrigir os erros materiais de períodos anteriores de forma retrospectiva, a partir da data em que tal erro foi identificado, salvo quando for impraticável determinar os efeitos específicos do período ou o efeito cumulativo do erro.

Está correto o que se afirma em

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956750

Contabilidade Pública

No que se refere a subvenções, considere:

I. As subvenções governamentais recebidas gratuitamente devem ser reconhecidas diretamente no patrimônio líquido da entidade.

II. As subvenções devem ser reconhecidas na demonstração do resultado nos períodos em que a entidade reconhece os custos relacionados à subvenção recebida.

III. A contrapartida da subvenção governamental registrada no ativo deve ser feita em conta específica do passivo, enquanto não atendidos os requisitos para reconhecimento da receita com subvenção na demonstração do resultado.

IV. Caso o valor da subvenção deva ser obrigatoriamente retido na entidade, tal valor, após transitar pela demonstração do resultado, deve ser contabilizado em conta apropriada do patrimônio líquido (reserva de incentivos fiscais) para comprovação dessa condição.

Está correto o que se afirma APENAS em

I. As subvenções governamentais recebidas gratuitamente devem ser reconhecidas diretamente no patrimônio líquido da entidade.

II. As subvenções devem ser reconhecidas na demonstração do resultado nos períodos em que a entidade reconhece os custos relacionados à subvenção recebida.

III. A contrapartida da subvenção governamental registrada no ativo deve ser feita em conta específica do passivo, enquanto não atendidos os requisitos para reconhecimento da receita com subvenção na demonstração do resultado.

IV. Caso o valor da subvenção deva ser obrigatoriamente retido na entidade, tal valor, após transitar pela demonstração do resultado, deve ser contabilizado em conta apropriada do patrimônio líquido (reserva de incentivos fiscais) para comprovação dessa condição.

Está correto o que se afirma APENAS em

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956749

Contabilidade Geral

A empresa Sol & Chuva S.A. adquiriu um imóvel em 31/12/2023 e o classificou como propriedade para investimento. O imóvel

foi adquirido da seguinte forma:

• Entrada, no valor de R$ 500.000.

• Parcela de R$ 1.120.000, para ser paga em 31/12/2024.

• Parcela de R$ 1.505.280, para ser paga em 31/12/2025.

Adicionalmente, a empresa incorreu nos seguintes gastos:

• Impostos e taxas para registro do imóvel: R$ 50.000

• Reformas necessárias para deixar o imóvel em condições de uso: R$ 200.000

O imóvel possui uma vida útil econômica estimada de 50 anos e a empresa definiu como política contábil o método do valor justo. Sabendo que, na data da aquisição do imóvel, a taxa de juros compostos era de 12% a.a., e que os valores justos do imóvel em 31/12/2024 e 31/12/2025 eram R$ 3.500.000 e R$ 3.300.000, respectivamente, a empresa Sol & Chuva S.A. reconheceu

• Entrada, no valor de R$ 500.000.

• Parcela de R$ 1.120.000, para ser paga em 31/12/2024.

• Parcela de R$ 1.505.280, para ser paga em 31/12/2025.

Adicionalmente, a empresa incorreu nos seguintes gastos:

• Impostos e taxas para registro do imóvel: R$ 50.000

• Reformas necessárias para deixar o imóvel em condições de uso: R$ 200.000

O imóvel possui uma vida útil econômica estimada de 50 anos e a empresa definiu como política contábil o método do valor justo. Sabendo que, na data da aquisição do imóvel, a taxa de juros compostos era de 12% a.a., e que os valores justos do imóvel em 31/12/2024 e 31/12/2025 eram R$ 3.500.000 e R$ 3.300.000, respectivamente, a empresa Sol & Chuva S.A. reconheceu

Ano: 2026

Banca:

FCC

Órgão:

SEFAZ-SP

Prova:

FCC - 2026 - SEFAZ-SP - Auditor Fiscal da Receita Estadual - AFRE - Gestão Tributária - Conhecimentos Específicos (P3) |

Q3956748

Contabilidade Geral

Texto associado

Atenção: Utilize os dados a seguir para responder à questão.

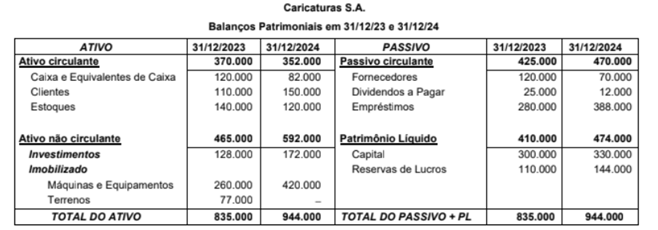

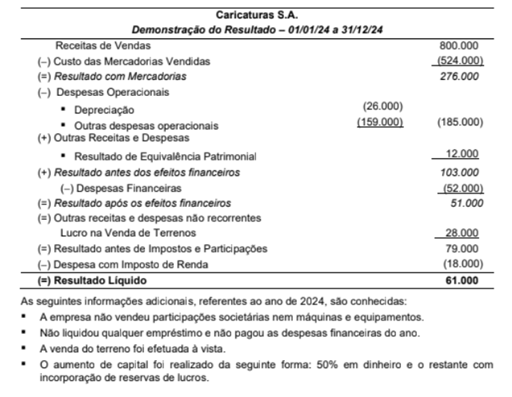

A empresa Caricaturas S.A. apresentou as seguintes demonstrações contábeis referentes ao ano de 2024:

O valor, em reais, correspondente ao Caixa das Atividades de Financiamentos é:

O valor, em reais, correspondente ao Caixa das Atividades de Investimentos é: