Selecionar segmento

Estude com questões de diferentes segmentos

Atenção: Isso limpará todos os campos já preenchidos no filtro!

Foram encontradas 1.600 questões

Resolva questões gratuitamente!

Junte-se a mais de 4 milhões de concurseiros!

Q1891978

Contabilidade Pública

Após receber algumas denúncias nos canais internos de

comunicação, uma autarquia federal resolveu criar um comitê

para verificar possíveis irregularidades na execução de contratos

vigentes do órgão com empresas de prestação de serviços

gráficos.

O controle exercido por essa autarquia na situação acima é do tipo:

O controle exercido por essa autarquia na situação acima é do tipo:

Q1891977

Administração Geral

Observe parte do organograma de um órgão público de controle a seguir.

Q1891976

Administração Geral

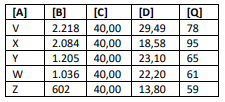

Em um hospital público, toda vez que o estoque de um

medicamento alcança um ponto crítico, o sistema emite uma

notificação para que o gestor responsável pelo estoque prepare

um pedido de compra, visando à reposição do medicamento. A

quantidade a ser comprada a cada pedido é definida conforme

informações abaixo. Por exemplo, quando a quantidade do

medicamento V atinge o seu ponto crítico, o gestor emite uma

ordem de compra de 78 unidades desse medicamento.

[A] = nome do medicamento

[B] = demanda anual do medicamento (em unidades)

[C] = custo de emissão do pedido de compra (em reais)

[D] = custo anual de estocagem (em reais)

[Q] = quantidade do medicamento a ser adquirida por ordem de compra (em unidades)

Sendo que

A técnica de gestão de estoques usada por esse hospital é o(a):

[A] = nome do medicamento

[B] = demanda anual do medicamento (em unidades)

[C] = custo de emissão do pedido de compra (em reais)

[D] = custo anual de estocagem (em reais)

[Q] = quantidade do medicamento a ser adquirida por ordem de compra (em unidades)

Sendo que

A técnica de gestão de estoques usada por esse hospital é o(a):

Q1891975

Administração Geral

No documento que formaliza o planejamento de uma entidade

governamental para os próximos dez anos consta o seguinte

objetivo:

“Fortalecer a difusão do conhecimento produzido na instituição ao público interno e externo, por meio de ações voltadas ao ensino e pesquisa.”

Quanto ao nível hierárquico, trata-se de um objetivo:

“Fortalecer a difusão do conhecimento produzido na instituição ao público interno e externo, por meio de ações voltadas ao ensino e pesquisa.”

Quanto ao nível hierárquico, trata-se de um objetivo:

Q1891974

Administração Geral

Um diretor de Recursos Humanos e sua equipe identificaram um

conjunto de alternativas cabíveis para a implementação da

gestão do desempenho no órgão, mas eles não conseguem

avaliar qual delas é a melhor.

A técnica de apoio à decisão que pode ajudar o diretor e sua equipe na situação acima é o(a):

A técnica de apoio à decisão que pode ajudar o diretor e sua equipe na situação acima é o(a):

Q1891973

Administração Geral

Frederico é coordenador de Tecnologia da Informação (TIC) em

um importante órgão da Administração Pública Federal.

Recentemente, ele participou de uma das mais importantes

conferências sobre inovações tecnológicas voltadas para o setor

público. Sua participação tinha como objetivo buscar informações

sobre novas tecnologias e analisar iniciativas de TIC de outros

órgãos a fim de comparar com as práticas internas do órgão em

que trabalha.

Ao participar da referida conferência, Frederico desempenhou o seguinte papel do administrador:

Ao participar da referida conferência, Frederico desempenhou o seguinte papel do administrador:

Q1891972

Administração Geral

Dois órgãos públicos, A e B, tinham um mesmo objetivo:

digitalizar todos os serviços por eles oferecidos ao público. Após

muitos estudos e reuniões de avaliação de alternativas, o órgão A

optou por abrir uma licitação para contratação de empresa

terceirizada que pudesse implementar a digitalização dos serviços

do órgão. Por outro lado, o órgão B decidiu abrir concurso

público para contratar profissionais da área de tecnologia da

informação capazes de executar o projeto de digitalização dos

serviços. Ao final do mesmo período, ambos os órgãos

conseguiram deixar seus serviços totalmente digitais.

Na Teoria dos Sistemas, o conceito que explica o fato de os órgãos A e B alcançarem o mesmo objetivo por caminhos diferentes é:

Na Teoria dos Sistemas, o conceito que explica o fato de os órgãos A e B alcançarem o mesmo objetivo por caminhos diferentes é:

Q1891971

Administração Geral

O gerente do setor de ouvidoria de um órgão público criou o

programa “Excelência no Atendimento”, cujo objetivo é

reconhecer a excelência e a qualidade do trabalho dos seus

funcionários. Os servidores que se destacam no atendimento aos

cidadãos que procuram a Ouvidoria do órgão são homenageados

pelo gerente em cerimônia pública, e recebem dele uma placa e

uma medalha de condecoração.

Na situação acima, o gerente exerce a função administrativa de:

Na situação acima, o gerente exerce a função administrativa de:

Q1891970

Administração Geral

Veja a seguir a tirinha do cartunista argentino Quino. Nela, o

termo “burocracia” está sendo usado com um sentido negativo.

Entretanto, conforme elucidado pelo sociólogo Robert Merton, o que é entendido como algo negativo na burocracia são suas disfunções, e não o modelo em si.

Nesse sentido, uma das disfunções da burocracia identificada por Merton é a:

Entretanto, conforme elucidado pelo sociólogo Robert Merton, o que é entendido como algo negativo na burocracia são suas disfunções, e não o modelo em si.

Nesse sentido, uma das disfunções da burocracia identificada por Merton é a:

Q1891969

Administração Geral

Em meio à adoção do teletrabalho, um departamento passou a

controlar o trabalho semanal de seus técnicos, conforme

apresentado na tabela a seguir.

Com base exclusivamente na tabela acima, o(a) técnico(a) com maior eficiência na Semana 1 foi:

Com base exclusivamente na tabela acima, o(a) técnico(a) com maior eficiência na Semana 1 foi:

Q1891968

Administração Financeira e Orçamentária

O Sistema de Controle Interno do Poder Executivo Federal é

formado por um órgão central, a Secretaria Federal de Controle

Interno, e por órgãos setoriais. A organização e as competências

dos órgãos do sistema são legalmente definidas.

A atuação dos órgãos setoriais do sistema decorrente das disposições legais:

A atuação dos órgãos setoriais do sistema decorrente das disposições legais:

Q1891967

Administração Financeira e Orçamentária

No arcabouço conceitual-normativo do orçamento público há

muitos conceitos associados à contabilidade. Quando se fala de

despesa contábil, por exemplo, tem-se a ideia de consumo de

recursos, com consequente redução patrimonial. Porém, no

orçamento público, a concepção de despesa tem uma

perspectiva diversa.

Esse entendimento é importante principalmente para a avaliação do impacto e dos desdobramentos da execução de despesas no patrimônio público.

Uma despesa orçamentária cujo reconhecimento diverge do conceito contábil de despesa pode ser ilustrada por:

Esse entendimento é importante principalmente para a avaliação do impacto e dos desdobramentos da execução de despesas no patrimônio público.

Uma despesa orçamentária cujo reconhecimento diverge do conceito contábil de despesa pode ser ilustrada por:

Q1891966

Administração Financeira e Orçamentária

Após o devido processo licitatório, uma entidade assinou um

contrato com uma empresa prestadora de serviço, detalhando

diretrizes e condições para a prestação do serviço pelo período

de um ano, conforme previsto no edital.

Por se tratar de uma despesa contratual, de acordo com as disposições normativas, quanto ao empenho de tal despesa:

Por se tratar de uma despesa contratual, de acordo com as disposições normativas, quanto ao empenho de tal despesa:

Q1891965

Administração Financeira e Orçamentária

A atividade de planejamento que dá suporte aos pilares do

orçamento público – receitas e despesas públicas – requer o uso

de informações de qualidade, para que seja efetiva como

ferramenta para o gestor público.

Uma etapa crucial na elaboração de qualquer orçamento é a previsão das receitas. Essa etapa antecede a fixação das despesas a serem incluídas no orçamento, além de ser base para se estimarem as necessidades de financiamento do governo.

Nessa etapa devem ser selecionadas informações relevantes e dispensadas aquelas que podem afetar a qualidade da previsão.

Uma informação que pode ser dispensada nessa etapa refere-se:

Uma etapa crucial na elaboração de qualquer orçamento é a previsão das receitas. Essa etapa antecede a fixação das despesas a serem incluídas no orçamento, além de ser base para se estimarem as necessidades de financiamento do governo.

Nessa etapa devem ser selecionadas informações relevantes e dispensadas aquelas que podem afetar a qualidade da previsão.

Uma informação que pode ser dispensada nessa etapa refere-se:

Q1891964

Administração Financeira e Orçamentária

Um servidor lotado em uma comissão de orçamento de um ente

legislativo estava tentando explicar para um parlamentar a

diferença entre despesas de capital que devem ser classificadas

como investimentos e aquelas que são tidas como inversões

financeiras. O parlamentar queria propor uma emenda ao

orçamento para uma despesa de capital do tipo inversão

financeira.

Uma característica das despesas classificáveis nesse grupo é:

Uma característica das despesas classificáveis nesse grupo é:

Q1891963

Administração Financeira e Orçamentária

As receitas são um dos pilares do orçamento público e sua

correta classificação contribui para gerar relatórios relevantes

para o processo de gestão pública. A classificação econômica das

receitas públicas apresenta as categorias correntes e de capital.

Ao examinar um relatório analítico de receitas ao final de um dado exercício para identificar eventuais inconsistências, um servidor técnico da área de controle deve considerar que:

Ao examinar um relatório analítico de receitas ao final de um dado exercício para identificar eventuais inconsistências, um servidor técnico da área de controle deve considerar que:

Q1891962

Administração Financeira e Orçamentária

Ao avaliar o texto e anexos da Lei Orçamentária Anual (LOA) de

um ente para um dado exercício, um servidor da área de controle

identificou um item que considerou incompatível para esse

instrumento. Porém, ao discutir o caso com outros colegas do seu

departamento, o servidor admitiu que estava equivocado.

O item identificado pelo servidor na análise da LOA refere-se:

O item identificado pelo servidor na análise da LOA refere-se:

Q1891961

Administração Financeira e Orçamentária

Um servidor alocado em uma unidade de controle interno de um

ente público estava avaliando a adequação das peças

orçamentárias, quando algo chamou a sua atenção ao analisar os

anexos da Lei de Diretrizes Orçamentárias do exercício vigente.

A ausência de item obrigatório no Anexo de Riscos Fiscais que pode ter chamado a atenção do servidor foi:

A ausência de item obrigatório no Anexo de Riscos Fiscais que pode ter chamado a atenção do servidor foi:

Q1891960

Administração Financeira e Orçamentária

O processo de planejamento no âmbito da administração pública

brasileira conta com instrumentos legais que, de forma integrada,

contribuem para a boa gestão dos recursos públicos. Um desses

instrumentos, o Plano Plurianual, é um dos mais desafiadores

quanto à elaboração e ao acompanhamento por parte dos órgãos

de controle e da sociedade.

Um elemento desse instrumento que dificulta a sua comparabilidade ao longo do tempo e com outros entes é:

Um elemento desse instrumento que dificulta a sua comparabilidade ao longo do tempo e com outros entes é:

Q1891959

Administração Financeira e Orçamentária

O orçamento pode ser considerado um instrumento básico de

ação no contexto da gestão pública. Sua elaboração e execução

devem seguir normas que assegurem a aplicação regular dos

recursos públicos.

Uma equipe de servidores responsável pela consolidação da proposta orçamentária de um ente público para um dado exercício deve considerar que o orçamento:

Uma equipe de servidores responsável pela consolidação da proposta orçamentária de um ente público para um dado exercício deve considerar que o orçamento: